Best Buy Now, Pay Later Services

Wagepay 🏆 2026

- See all

Really frustrating. Have sent multiple emails, and only got a robot reply. Have been trying for 2 weeks now. Payment is due next week and i have heard nothing with no help. Really disappointing

Zip Pay 🏆 2026

- See all

I needed to change my name and thought it would be a difficult process, I worked with a lady Nirwana, she made it a very easy process for me and once… Read more

I’d submitted the correct documents my name was changed back to my maiden name! Nirwana was very helpful and kind. Thanks so much for your help Nirwana, you made the transition very easy for me!!

deferit

- See all

They are awesome and when you think you can pay them on a certain date and need more time they let you. And if you have any issues they fix the problem quickly. 10/10

Afterpay

- See all

credit check without my consent, which was not reported to me as customer.

Property Credit

The service provided was excellent, professional and prompt! The customer was very friendly and helpful with each step of the process. I would highly recommend Property Credit and would use their services again!

Gimmie

Not happy with customer service or support.unable to contact by phone as you only get a message service, leave a message and then no return calls.… Read more

Emails just as bad. Asked for balance of account then when I get close to the finish date I get an email stating I owe more. I query this and get told sorry error in system. Again this keeps happening. When your unable to speak to someone or get a proper response then it's not worth using a company like this. Not happy

NAB Buy Now Pay Later

I am a NAB customer. Recently NAB release its Now Pay Later Visa card which splits payments into 4 fortnights with no interest. Recently I’ve been… Read more

using NAB more and more because of the value I get. NAB goodies are similar to AMEX and other credit providers offering cash back or discounts albeit for lower value purchases. I have saved a lot of money from internet service provider, fuel and shopping. I’ve stopped using Afterpay as frequently as I used to. If Afterpay doesn’t get on board with these sort of spend incentives it will be a tough environment to compete.

Klarna

- See all

Am being charged $200 for orders never made, being told contact the company and prove i never made the order I sent screen shots but thats not enough… Read more

Yes its been helpful for large orders that I MADE...$200 for orders that were never made and trying to get a refund for the first payment and putting an end to the following payments is a process and its not happening, because despite screenshots i cant prove anything

Laybuy

10000 PERCENT! this COMPANY is FRAUDULENT! I just saw my credit score went down by 4 points for a new enquiry with LAYBUY on the 24 of May 2025,… Read more

that I didn't do. I KNOW THEY DID IT LOL I signed up with them in 2021 and I didn't end up using them. Customer service is useless, it doesn't exist. How can I raise a dispute with LAYBUY when it's a GHOST. Stay away from this SHAAAADY ASSS COMPANY, don't even think about signing up unless you want to see your credit score randomly get enquires from them LOL What a joke! Hope they are being investigated.

Pay It Later

Saved by the unfortunate ones who left a review to save more people from losing – Omg I seriously never both to check out reviews for some reason it was the first thing on google search so I clicked on it and how lucky that I did… Read more

. I'm so sorry to all the customers that have had money stolen an their identity stolen a huge sorry to all the small businesses ripped off an then made to look like the bad guys with the ppl who purchased off U an hadn't found out why their goods never arrived . They seriously need some karma to come get them

Shop Pay

Allows scammers to operate and rip people off. Then will not respond to emails regarding complaint.

Wizpay

- See all

Steer Clear – Scammers! Steer clear as you will just be giving up your information to be sold onto other companies.

Westpac PartPay

Like others here it’s an extremely confusing process made out to look simplistic when really it’s just more or less using the regular features of… Read more

your credit card. Your credit card is still charged as normal, it’ll just set up some regular direct debits. Useless product.

RapidPay

Payright

Payright is not interest free but misleading – I recently financed a solar installation through Payright, and the experience has been far from satisfactory. The total cost of the installation was… Read more

$11,700. Payright disbursed $10,720.72 to the vendor, yet I was charged a total of $13,787.95. This includes an additional charge of $3,067.23, which represents approximately 29% over the original amount.

On top of that, when factoring in the account fees over the 5-year term, the total effective charge comes to roughly 8%. This is especially concerning given that the financing was marketed as interest-free.

I feel completely misled by this arrangement, and it seems like an unfair and deceptive practice. Be cautious if you're considering using Payright—what looks like an interest-free deal may turn out to be far more costly than you expected

How does Buy Now, Pay Later work?

These services allow you to make purchases and receive the product instantly without paying the full price upfront, instead paying it later in regular, scheduled interest-free instalments over a certain amount of time.

They are easier and quicker to sign up for in comparison to credit cards or debit cards, and in most cases you are not required to provide proof of income or undergo a credit check to be approved.

At the moment, AfterPay and Zip are leading the way as most popular ‘Buy Now, Pay Later’ services in Australia. There are many other companies offering similar services, all with slight variances in joining requirements, the flexibility of payment schedules and additional fees. It’s important to know all the terms and conditions that come with each service so you don’t get hit with any unexpected fees.

Should I use a Buy Now, Pay Later Service?

Arguments in favour of using one

These ‘Buy Now, Pay Later’ services can be an easy way to spread out the burden of making payments, and if you are on top of your spending, you won’t get hit with any extra fees.

So if you are already good at managing your finances, and plan on using it for things you would be purchasing regardless, it can be a relatively safe option and and a good interest-free alternative to credit cards, and help you avoid credit card debt.

When a Buy Now, Pay Later Service may not be for you

However, there are some risks that come with using these services, especially if you don’t manage your payments or something unexpected stops you from earning an income.

BNPL services can be very appealing to someone working on a casual or part-time basis, as the repayments can match up with a weekly or fortnightly salary cycle. However, someone in this position may also be at risk or running up late fees due to unreliable income if they lose a shift one week or have their hours permanently reduced.

People are more likely to buy more than they usually would and overspend when using Buy Now, Pay Later services because they are able to break up the payment, and it can have a negative impact on your financial future.

On top of fees you receive for late or rejected payments, excessive purchases and missed payments can affect your credit score, and consequently your ability to secure a loan. So if you already have trouble managing finances and payments, these services may not be appropriate for you.

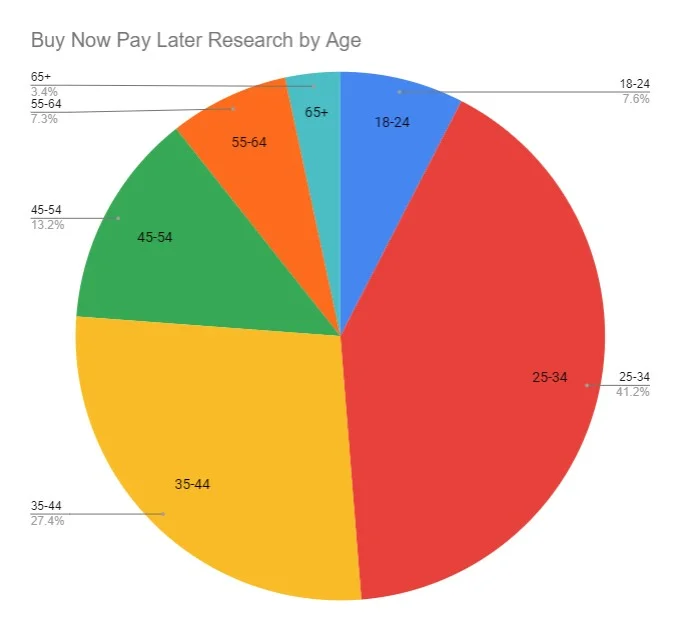

What percentage of people use Buy Now, Pay Later Services?

These services are most popular with people in their mid-20s to mid-30s, with this cohort making up over 40% of people who research Buy Now Pay Later services on ProductReview.com.au. From all age groups, women show slightly more interest in the service than men, accounting for 55% of visitors to relevant pages.

Payment Schedules and Instalments

AfterPay

Credit check and spend limit

AfterPay does not require a credit check to sign up, only a verification of identity. You must be at least 18-years old to sign up, and have an eligible debit or credit card to apply.

There is no hard limit on spending, and your allowable spending limit increases gradually over time.

Fortnightly repayments

Using AfterPay, you're able to break your payment into four fortnightly instalments, with the first instalment paid at the time of purchase. There is no flexibility in changing how much each payment is, or how often you make them.

How do you use the pay later option?

The AfterPay service is available both online and in-store. When paying online you select the AfterPay option at checkout. In store, simply scan the barcode on the AfterPay app at the counter of merchants who use the service.

Zip

Zip offers two different levels of payment programs to suit your level of purchase: Zip Pay and Zip Money.

Credit check and Eligibility

Zip does conduct credit checks on some customers.

- Zip Pay only requires a phone number and linked Facebook, Paypal or LinkedIn account.

- Zip Money asks for your address, employment status, income statement, and transaction history in order to be approved.

Establishment fees

Zip Pay is free to join. Since Zip Money offers larger account credit for purchases, it incurs an establishment fee of between $25 and $299 depending on your credit limit.

Spend limit

The main difference between Zip Pay and Zip Money is that Zip Pay allows you to make purchases of up to $1,000, whereas Zip Money is for purchases between $1,000 to $5,000. The monthly limit will depend on your credit limit and will vary according to your contract.

Interest

Zip Pay is interest-free. Payments in the Zip Money plan are interest-free for the first three months of each purchase.

After three months, you'll pay interest of 19.9% p,a. Minimum repayment ranges from $40 to $299 each month, or a percentage of your balance owing, whichever is greater.

Flexible repayment options

One advantage Zip has over AfterPay is the flexibility it offers with payment plans: you have the option to set up weekly, fortnightly or monthly repayment schedules that suit you.

The only requirement is a minimum payment of $10 per week or $40 a month.

Additional Fees and Missed Payments

All ‘Buy Now, Pay Later Services’ charge a late fee if you miss a payment, it’s how they make a profit without charging interest. Each company has different fees and conditions, so make sure you read into them before choosing a service.

AfterPay

AfterPay is free to use as long as you don’t miss any payments. It has zero interest, and no joining fees.

What happens if I miss an Afterpay payment?

For late fees on purchase amounts $40 or under, you are charged a $10 late fee if you miss an automatic payment, followed by a $7 fee if you fail to repay that missed instalment within 7 days of the due date.

For orders between $40 and $272, the late fee is capped at 25% of the purchase price.

For purchase amounts over $272, this late fee is capped at 25% of the purchase price or $68, whichever is less.

If you miss a payment, your account is suspended and you cannot use AfterPay on any new purchases until your payments are up to date.

Hardship policy

AfterPay also have a Hardship Policy to help you out if something unexpected happens to you or your circumstances change.

Assessed on a case-by-case basis, it gives you the possibility to come up with a new payment plan, extend the term of your payment arrangement so you can make smaller payments over a longer period, or avoid extra fees.

It offers support to people in a range of circumstances caused by: COVID-19, natural disasters, redundancy, recent unemployment, sudden illness, relationship breakdown and other personal reasons.

Zip

Zip charges a $6 monthly account fee if you have a balance, but this fee is waived if the closing balance is paid by the due date.

If you use Zip Pay or Zip Money to pay bills you’ll be charged a 1.5% payment processing fee.

Late and dishonour fees

If the minimum repayment amount is not paid within 21 days after the due date, a late fee will be charged - $5 for Zip Pay, and $15 for Zip Money. Zip also charges ‘dishonour’ fees, charged if a scheduled payment was rejected by the bank due to insufficient funds or incorrect bank account details.

Hardship policy

Like AfterPay, Zip also has a hardship policy. It takes into account individual circumstances such as: income changes, recently losing a job or having hours cut back, a relationship breakdown, injury, illness, natural disasters or other emergencies.

A request for hardship assistance is not a given; Zip will assess on a case-by-case basis. If it decides to help, Zip may devise a temporary alternative payment arrangement until you can resume your normal payments.

Terms and Conditions

While most information is available on the Zip website, Zip do not make their Terms & Conditions readily available for public viewing. This makes it different from AfterPay, and here Zip loses some points in the transparency department.

Other Options

Latitude Pay and Openpay are more recent additions to the interest-free payment market, offering similar programs to AfterPay and Zip.

Latitude Pay

Latitude Pay gives you interest-free payments of up to $1,000. The automatic plan is set to 10-week instalments, so you only pay 10% up front and the remaining in 9 weekly instalments.

You also have the option to pay your balance off at an earlier date. They do conduct credit checks during your application, and charge late fees of $10 for purchases less than $50, and $50 for purchases up to $1,000.

Openpay

Openpay has more fees compared to other 'Buy Now, Pay Later’ services. There is an establishment fee to set up your account, a plan management fee and redraw fee that applies to some plans. The missed payment fee is $9.50, and if you fail to pay that missed instalment 8 days after your due date, it's an additional $19.50.

If you make a return or get a refund, you don’t get the plan management fee refunded, so better off going for something that doesn’t charge instalment fees at all.

The bottom line

Overall, choosing to sign up with a Buy Now, Pay Later service may seem like a convenient solution as a shopper that's too good to pass up.

However, it's important to be aware of the financial implications in the event that you can't make repayments on time. Entering into a contract knowing the terms and conditions, and knowing you can afford any financial penalties should they arise, can help give you peace of mind that a BNPL service is right for you.

Disclaimer: The information on this website is for general information only. It should not be taken as constituting professional advice from the website owner - ProductReview.com.au. ProductReview.com.au is not a financial adviser. You should consider seeking independent legal, financial, taxation or other advice to check how the website information relates to your unique circumstances. ProductReview.com.au is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by use of this website.